Sure, in aggregate, across all homeowners, they pay out less then they take in. But that doesn’t make it a scam. They can pay out more for a specific homeowner than they take in.

On average, you will be worse off if you buy insurance than if you don’t. The odds are against the buyer with insurance.

However, if you have a utility function that isn’t linear in the amount of money you have, it can be advantageous to get insurance. Say you don’t care that much about having the small amount of extra money you’d have if you avoided insurance, but you care very, very much about losing the value of your house at one go. Insurance will mitigate that risk.

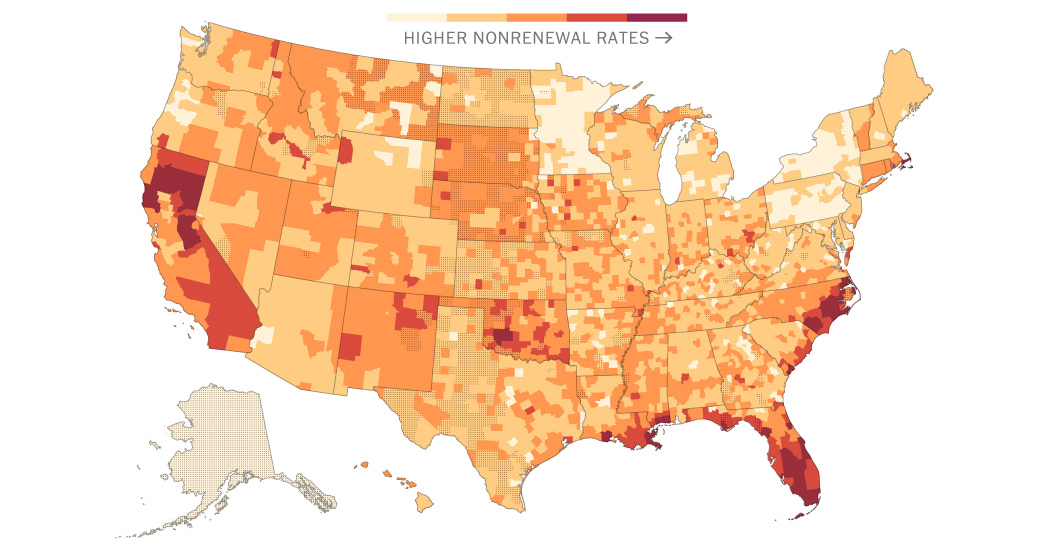

If you have enough reasonably-liquid assets that you can afford to just replace your house with cash, you might want to not get insurance. But even in that case, you’d need to hold assets in a liquid form, which places constraints on those assets. Let’s say that the average number of houses that burns down in a state per year is 100. You could have every homeowner ensure that they have enough liquid assets to replace their house. But it’d be cheaper to have an insurer hold, say, 500 times the cost of a house in liquid assets. They couldn’t cover the situation where all the houses burn down, and this is why insurers typically don’t offer coverage for correlated risk scenarios, where all houses might be impacted, as in war. But for things like fires, it’d be extraordinarily unlikely for more than five times the normal amount to burn down, so having an insurer involved relaxes constraints on how assets are held and how much need to be held.

NPR Planet Money did a bit on correlated risk in homeowner’s insurance a while back.

Sure, in aggregate, across all homeowners, they pay out less then they take in. But that doesn’t make it a scam. They can pay out more for a specific homeowner than they take in.

On average, you will be worse off if you buy insurance than if you don’t. The odds are against the buyer with insurance.

However, if you have a utility function that isn’t linear in the amount of money you have, it can be advantageous to get insurance. Say you don’t care that much about having the small amount of extra money you’d have if you avoided insurance, but you care very, very much about losing the value of your house at one go. Insurance will mitigate that risk.

If you have enough reasonably-liquid assets that you can afford to just replace your house with cash, you might want to not get insurance. But even in that case, you’d need to hold assets in a liquid form, which places constraints on those assets. Let’s say that the average number of houses that burns down in a state per year is 100. You could have every homeowner ensure that they have enough liquid assets to replace their house. But it’d be cheaper to have an insurer hold, say, 500 times the cost of a house in liquid assets. They couldn’t cover the situation where all the houses burn down, and this is why insurers typically don’t offer coverage for correlated risk scenarios, where all houses might be impacted, as in war. But for things like fires, it’d be extraordinarily unlikely for more than five times the normal amount to burn down, so having an insurer involved relaxes constraints on how assets are held and how much need to be held.

NPR Planet Money did a bit on correlated risk in homeowner’s insurance a while back.

https://www.npr.org/transcripts/349650496

Exactly. Insurance handles low-probability high-impact uncorrelated disasters really nicely, and is worth paying for to protect against those.

Correlated disasters require public policy and shared infrastructure to lower their risk and the extent to which people are exposed to them.